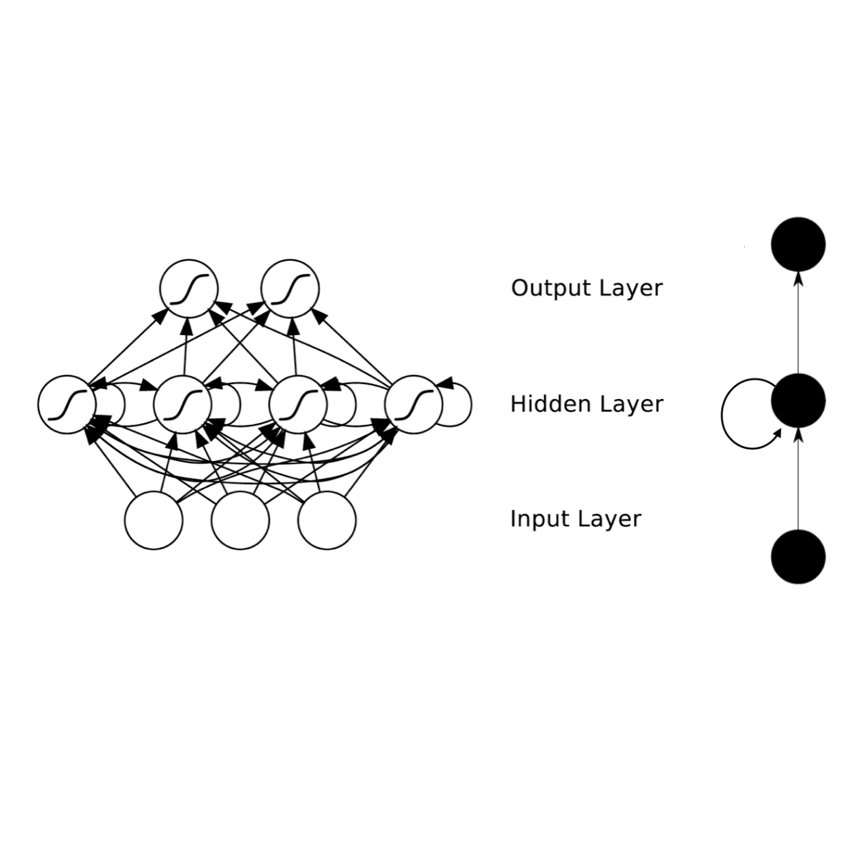

This study examines the use of a recurrent neural network for estimating the parameters of a Hawkes model based on high-frequency financial data, and subsequently, for computing volatility. Neural networks have shown promising results in various fields, and interest in finance is also growing. Our approach demonstrates significantly faster computational performance compared to traditional maximum likelihood estimation methods while yielding comparable accuracy in both simulation and empirical studies. Furthermore, we demonstrate the application of this method for real-time volatility measurement, enabling the continuous estimation of financial volatility as new price data keeps coming from the market.

相關內容

ChatGPT has demonstrated remarkable capabilities across various natural language processing (NLP) tasks. However, its potential for inferring dynamic network structures from temporal textual data, specifically financial news, remains an unexplored frontier. In this research, we introduce a novel framework that leverages ChatGPT's graph inference capabilities to enhance Graph Neural Networks (GNN). Our framework adeptly extracts evolving network structures from textual data, and incorporates these networks into graph neural networks for subsequent predictive tasks. The experimental results from stock movement forecasting indicate our model has consistently outperformed the state-of-the-art Deep Learning-based benchmarks. Furthermore, the portfolios constructed based on our model's outputs demonstrate higher annualized cumulative returns, alongside reduced volatility and maximum drawdown. This superior performance highlights the potential of ChatGPT for text-based network inferences and underscores its promising implications for the financial sector.

Currently, the wide spreading of real-time applications such as VoIP and videos-based applications require more data rates and reduced latency to ensure better quality of service (QoS). A well-designed traffic classification mechanism plays a major role for good QoS provision and network security verification. Port-based approaches and deep packet inspections (DPI) techniques have been used to classify and analyze network traffic flows. However, none of these methods can cope with the rapid growth of network traffic due to the increasing number of Internet users and the growth of real time applications. As a result, these methods lead to network congestion, resulting in packet loss, delay and inadequate QoS delivery. Recently, a deep learning approach has been explored to address the time-consumption and impracticality gaps of the above methods and maintain existing and future traffics of real-time applications. The aim of this research is then to design a dynamic traffic classifier that can detect elephant flows to prevent network congestion. Thus, we are motivated to provide efficient bandwidth and fast transmision requirements to many Internet users using SDN capability and the potential of Deep Learning. Specifically, DNN, CNN, LSTM and Deep autoencoder are used to build elephant detection models that achieve an average accuracy of 99.12%, 98.17%, and 98.78%, respectively. Deep autoencoder is also one of the promising algorithms that does not require human class labeler. It achieves an accuracy of 97.95% with a loss of 0.13 . Since the loss value is closer to zero, the performance of the model is good. Therefore, the study has a great importance to Internet service providers, Internet subscribers, as well as for future researchers in this area.

Graph classification aims to categorise graphs based on their structure and node attributes. In this work, we propose to tackle this task using tools from graph signal processing by deriving spectral features, which we then use to design two variants of Gaussian process models for graph classification. The first variant uses spectral features based on the distribution of energy of a node feature signal over the spectrum of the graph. We show that even such a simple approach, having no learned parameters, can yield competitive performance compared to strong neural network and graph kernel baselines. A second, more sophisticated variant is designed to capture multi-scale and localised patterns in the graph by learning spectral graph wavelet filters, obtaining improved performance on synthetic and real-world data sets. Finally, we show that both models produce well calibrated uncertainty estimates, enabling reliable decision making based on the model predictions.

A key feature of out-of-distribution (OOD) detection is to exploit a trained neural network by extracting statistical patterns and relationships through the multi-layer classifier to detect shifts in the expected input data distribution. Despite achieving solid results, several state-of-the-art methods rely on the penultimate or last layer outputs only, leaving behind valuable information for OOD detection. Methods that explore the multiple layers either require a special architecture or a supervised objective to do so. This work adopts an original approach based on a functional view of the network that exploits the sample's trajectories through the various layers and their statistical dependencies. It goes beyond multivariate features aggregation and introduces a baseline rooted in functional anomaly detection. In this new framework, OOD detection translates into detecting samples whose trajectories differ from the typical behavior characterized by the training set. We validate our method and empirically demonstrate its effectiveness in OOD detection compared to strong state-of-the-art baselines on computer vision benchmarks.

The neural Ordinary Differential Equation (ODE) model has shown success in learning complex continuous-time processes from observations on discrete time stamps. In this work, we consider the modeling and forecasting of time series data that are non-stationary and may have sharp changes like spikes. We propose an RNN-based model, called RNN-ODE-Adap, that uses a neural ODE to represent the time development of the hidden states, and we adaptively select time steps based on the steepness of changes of the data over time so as to train the model more efficiently for the "spike-like" time series. Theoretically, RNN-ODE-Adap yields provably a consistent estimation of the intensity function for the Hawkes-type time series data. We also provide an approximation analysis of the RNN-ODE model showing the benefit of adaptive steps. The proposed model is demonstrated to achieve higher prediction accuracy with reduced computational cost on simulated dynamic system data and point process data and on a real electrocardiography dataset.

Modern scientific problems are often multi-disciplinary and require integration of computer models from different disciplines, each with distinct functional complexities, programming environments, and computation times. Linked Gaussian process (LGP) emulation tackles this challenge through a divide-and-conquer strategy that integrates Gaussian process emulators of the individual computer models in a network. However, the required stationarity of the component Gaussian process emulators within the LGP framework limits its applicability in many real-world applications. In this work, we conceptualize a network of computer models as a deep Gaussian process with partial exposure of its hidden layers. We develop a method for inference for these partially exposed deep networks that retains a key strength of the LGP framework, whereby each model can be emulated separately using a DGP and then linked together. We show in both synthetic and empirical examples that our linked deep Gaussian process emulators exhibit significantly better predictive performance than standard LGP emulators in terms of accuracy and uncertainty quantification. They also outperform single DGPs fitted to the network as a whole because they are able to integrate information from the partially exposed hidden layers. Our methods are implemented in an R package $\texttt{dgpsi}$ that is freely available on CRAN.

Using a perturbation technique, we derive a new approximate filtering and smoothing methodology generalizing along different directions several existing approaches to robust filtering based on the score and the Hessian matrix of the observation density. The main advantages of the methodology can be summarized as follows: (i) it relaxes the critical assumption of a Gaussian prior distribution for the latent states underlying such approaches; (ii) can be applied to a general class of state-space models including univariate and multivariate location, scale and count data models; (iii) has a very simple structure based on forward-backward recursions similar to the Kalman filter and smoother; (iv) allows a straightforward computation of confidence bands around the state estimates reflecting the combination of parameter and filtering uncertainty. We show through an extensive Monte Carlo study that the mean square loss with respect to exact simulation-based methods is small in a wide range of scenarios. We finally illustrate empirically the application of the methodology to the estimation of stochastic volatility and correlations in financial time-series.

Diffusion models are a class of deep generative models that have shown impressive results on various tasks with dense theoretical founding. Although diffusion models have achieved impressive quality and diversity of sample synthesis than other state-of-the-art models, they still suffer from costly sampling procedure and sub-optimal likelihood estimation. Recent studies have shown great enthusiasm on improving the performance of diffusion model. In this article, we present a first comprehensive review of existing variants of the diffusion models. Specifically, we provide a first taxonomy of diffusion models and categorize them variants to three types, namely sampling-acceleration enhancement, likelihood-maximization enhancement and data-generalization enhancement. We also introduce in detail other five generative models (i.e., variational autoencoders, generative adversarial networks, normalizing flow, autoregressive models, and energy-based models), and clarify the connections between diffusion models and these generative models. Then we make a thorough investigation into the applications of diffusion models, including computer vision, natural language processing, waveform signal processing, multi-modal modeling, molecular graph generation, time series modeling, and adversarial purification. Furthermore, we propose new perspectives pertaining to the development of this generative model.

As soon as abstract mathematical computations were adapted to computation on digital computers, the problem of efficient representation, manipulation, and communication of the numerical values in those computations arose. Strongly related to the problem of numerical representation is the problem of quantization: in what manner should a set of continuous real-valued numbers be distributed over a fixed discrete set of numbers to minimize the number of bits required and also to maximize the accuracy of the attendant computations? This perennial problem of quantization is particularly relevant whenever memory and/or computational resources are severely restricted, and it has come to the forefront in recent years due to the remarkable performance of Neural Network models in computer vision, natural language processing, and related areas. Moving from floating-point representations to low-precision fixed integer values represented in four bits or less holds the potential to reduce the memory footprint and latency by a factor of 16x; and, in fact, reductions of 4x to 8x are often realized in practice in these applications. Thus, it is not surprising that quantization has emerged recently as an important and very active sub-area of research in the efficient implementation of computations associated with Neural Networks. In this article, we survey approaches to the problem of quantizing the numerical values in deep Neural Network computations, covering the advantages/disadvantages of current methods. With this survey and its organization, we hope to have presented a useful snapshot of the current research in quantization for Neural Networks and to have given an intelligent organization to ease the evaluation of future research in this area.

Deep learning (DL) based semantic segmentation methods have been providing state-of-the-art performance in the last few years. More specifically, these techniques have been successfully applied to medical image classification, segmentation, and detection tasks. One deep learning technique, U-Net, has become one of the most popular for these applications. In this paper, we propose a Recurrent Convolutional Neural Network (RCNN) based on U-Net as well as a Recurrent Residual Convolutional Neural Network (RRCNN) based on U-Net models, which are named RU-Net and R2U-Net respectively. The proposed models utilize the power of U-Net, Residual Network, as well as RCNN. There are several advantages of these proposed architectures for segmentation tasks. First, a residual unit helps when training deep architecture. Second, feature accumulation with recurrent residual convolutional layers ensures better feature representation for segmentation tasks. Third, it allows us to design better U-Net architecture with same number of network parameters with better performance for medical image segmentation. The proposed models are tested on three benchmark datasets such as blood vessel segmentation in retina images, skin cancer segmentation, and lung lesion segmentation. The experimental results show superior performance on segmentation tasks compared to equivalent models including U-Net and residual U-Net (ResU-Net).

小貼士

登錄享

注冊地址: 北京市海淀區羊坊店路18號2幢3層301-191