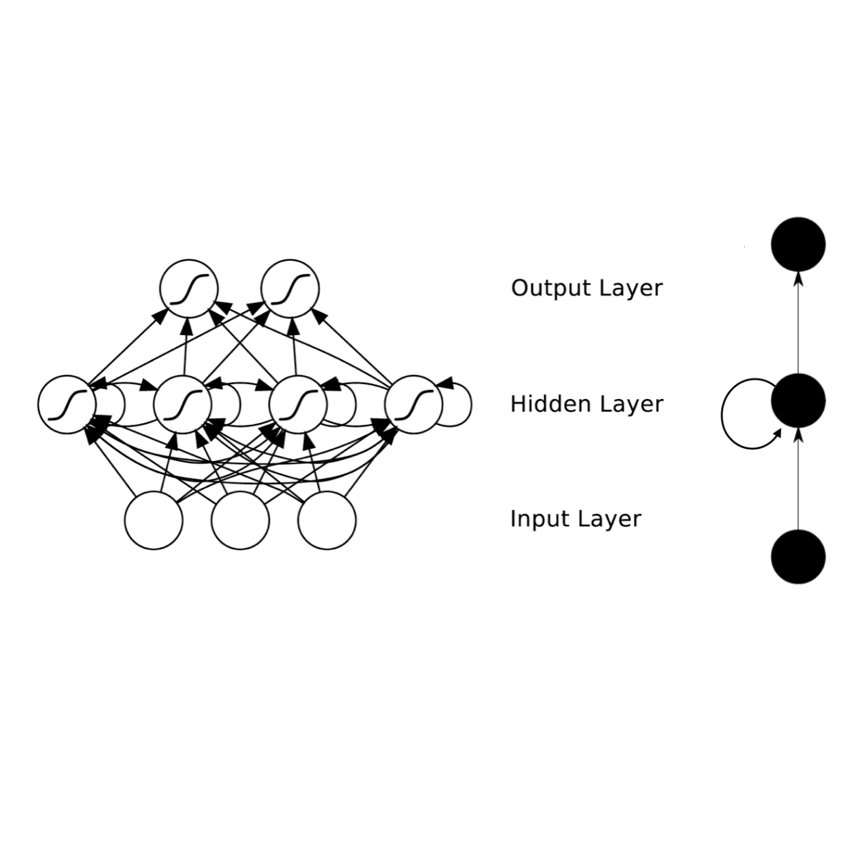

The Stochastic Volatility (SV) model and its variants are widely used in the financial sector while recurrent neural network (RNN) models are successfully used in many large-scale industrial applications of Deep Learning. Our article combines these two methods in a non-trivial way and proposes a model, which we call the Statistical Recurrent Stochastic Volatility (SR-SV) model, to capture the dynamics of stochastic volatility. The proposed model is able to capture complex volatility effects (e.g., non-linearity and long-memory auto-dependence) overlooked by the conventional SV models, is statistically interpretable and has an impressive out-of-sample forecast performance. These properties are carefully discussed and illustrated through extensive simulation studies and applications to five international stock index datasets: The German stock index DAX30, the Hong Kong stock index HSI50, the France market index CAC40, the US stock market index SP500 and the Canada market index TSX250. An user-friendly software package together with the examples reported in the paper are available at \url{//github.com/vbayeslab}.

相關內容

Escaping from saddle points and finding local minimum is a central problem in nonconvex optimization. Perturbed gradient methods are perhaps the simplest approach for this problem. However, to find $(\epsilon, \sqrt{\epsilon})$-approximate local minima, the existing best stochastic gradient complexity for this type of algorithms is $\tilde O(\epsilon^{-3.5})$, which is not optimal. In this paper, we propose LENA (Last stEp shriNkAge), a faster perturbed stochastic gradient framework for finding local minima. We show that LENA with stochastic gradient estimators such as SARAH/SPIDER and STORM can find $(\epsilon, \epsilon_{H})$-approximate local minima within $\tilde O(\epsilon^{-3} + \epsilon_{H}^{-6})$ stochastic gradient evaluations (or $\tilde O(\epsilon^{-3})$ when $\epsilon_H = \sqrt{\epsilon}$). The core idea of our framework is a step-size shrinkage scheme to control the average movement of the iterates, which leads to faster convergence to the local minima.

Stein variational gradient descent (SVGD) is a general-purpose optimization-based sampling algorithm that has recently exploded in popularity, but is limited by two issues: it is known to produce biased samples, and it can be slow to converge on complicated distributions. A recently proposed stochastic variant of SVGD (sSVGD) addresses the first issue, producing unbiased samples by incorporating a special noise into the SVGD dynamics such that asymptotic convergence is guaranteed. Meanwhile, Stein variational Newton (SVN), a Newton-like extension of SVGD, dramatically accelerates the convergence of SVGD by incorporating Hessian information into the dynamics, but also produces biased samples. In this paper we derive, and provide a practical implementation of, a stochastic variant of SVN (sSVN) which is both asymptotically correct and converges rapidly. We demonstrate the effectiveness of our algorithm on a difficult class of test problems -- the Hybrid Rosenbrock density -- and show that sSVN converges using three orders of magnitude fewer gradient evaluations of the log likelihood than its stochastic SVGD counterpart. Our results show that sSVN is a promising approach to accelerating high-precision Bayesian inference tasks with modest-dimension, $d\sim\mathcal{O}(10)$.

Stochastic partial differential equations (SPDEs) are the mathematical tool of choice for modelling spatiotemporal PDE-dynamics under the influence of randomness. Based on the notion of mild solution of an SPDE, we introduce a novel neural architecture to learn solution operators of PDEs with (possibly stochastic) forcing from partially observed data. The proposed Neural SPDE model provides an extension to two popular classes of physics-inspired architectures. On the one hand, it extends Neural CDEs and variants -- continuous-time analogues of RNNs -- in that it is capable of processing incoming sequential information arriving irregularly in time and observed at arbitrary spatial resolutions. On the other hand, it extends Neural Operators -- generalizations of neural networks to model mappings between spaces of functions -- in that it can parameterize solution operators of SPDEs depending simultaneously on the initial condition and a realization of the driving noise. By performing operations in the spectral domain, we show how a Neural SPDE can be evaluated in two ways, either by calling an ODE solver (emulating a spectral Galerkin scheme), or by solving a fixed point problem. Experiments on various semilinear SPDEs, including the stochastic Navier-Stokes equations, demonstrate how the Neural SPDE model is capable of learning complex spatiotemporal dynamics in a resolution-invariant way, with better accuracy and lighter training data requirements compared to alternative models, and up to 3 orders of magnitude faster than traditional solvers.

Many recent state-of-the-art (SOTA) optical flow models use finite-step recurrent update operations to emulate traditional algorithms by encouraging iterative refinements toward a stable flow estimation. However, these RNNs impose large computation and memory overheads, and are not directly trained to model such stable estimation. They can converge poorly and thereby suffer from performance degradation. To combat these drawbacks, we propose deep equilibrium (DEQ) flow estimators, an approach that directly solves for the flow as the infinite-level fixed point of an implicit layer (using any black-box solver), and differentiates through this fixed point analytically (thus requiring $O(1)$ training memory). This implicit-depth approach is not predicated on any specific model, and thus can be applied to a wide range of SOTA flow estimation model designs. The use of these DEQ flow estimators allows us to compute the flow faster using, e.g., fixed-point reuse and inexact gradients, consumes $4\sim6\times$ times less training memory than the recurrent counterpart, and achieves better results with the same computation budget. In addition, we propose a novel, sparse fixed-point correction scheme to stabilize our DEQ flow estimators, which addresses a longstanding challenge for DEQ models in general. We test our approach in various realistic settings and show that it improves SOTA methods on Sintel and KITTI datasets with substantially better computational and memory efficiency.

Momentum methods, including heavy-ball~(HB) and Nesterov's accelerated gradient~(NAG), are widely used in training neural networks for their fast convergence. However, there is a lack of theoretical guarantees for their convergence and acceleration since the optimization landscape of the neural network is non-convex. Nowadays, some works make progress towards understanding the convergence of momentum methods in an over-parameterized regime, where the number of the parameters exceeds that of the training instances. Nonetheless, current results mainly focus on the two-layer neural network, which are far from explaining the remarkable success of the momentum methods in training deep neural networks. Motivated by this, we investigate the convergence of NAG with constant learning rate and momentum parameter in training two architectures of deep linear networks: deep fully-connected linear neural networks and deep linear ResNets. Based on the over-parameterization regime, we first analyze the residual dynamics induced by the training trajectory of NAG for a deep fully-connected linear neural network under the random Gaussian initialization. Our results show that NAG can converge to the global minimum at a $(1 - \mathcal{O}(1/\sqrt{\kappa}))^t$ rate, where $t$ is the iteration number and $\kappa > 1$ is a constant depending on the condition number of the feature matrix. Compared to the $(1 - \mathcal{O}(1/{\kappa}))^t$ rate of GD, NAG achieves an acceleration over GD. To the best of our knowledge, this is the first theoretical guarantee for the convergence of NAG to the global minimum in training deep neural networks. Furthermore, we extend our analysis to deep linear ResNets and derive a similar convergence result.

We propose a stochastic conditional gradient method (CGM) for minimizing convex finite-sum objectives formed as a sum of smooth and non-smooth terms. Existing CGM variants for this template either suffer from slow convergence rates, or require carefully increasing the batch size over the course of the algorithm's execution, which leads to computing full gradients. In contrast, the proposed method, equipped with a stochastic average gradient (SAG) estimator, requires only one sample per iteration. Nevertheless, it guarantees fast convergence rates on par with more sophisticated variance reduction techniques. In applications we put special emphasis on problems with a large number of separable constraints. Such problems are prevalent among semidefinite programming (SDP) formulations arising in machine learning and theoretical computer science. We provide numerical experiments on matrix completion, unsupervised clustering, and sparsest-cut SDPs.

A High-dimensional and sparse (HiDS) matrix is frequently encountered in a big data-related application like an e-commerce system or a social network services system. To perform highly accurate representation learning on it is of great significance owing to the great desire of extracting latent knowledge and patterns from it. Latent factor analysis (LFA), which represents an HiDS matrix by learning the low-rank embeddings based on its observed entries only, is one of the most effective and efficient approaches to this issue. However, most existing LFA-based models perform such embeddings on a HiDS matrix directly without exploiting its hidden graph structures, thereby resulting in accuracy loss. To address this issue, this paper proposes a graph-incorporated latent factor analysis (GLFA) model. It adopts two-fold ideas: 1) a graph is constructed for identifying the hidden high-order interaction (HOI) among nodes described by an HiDS matrix, and 2) a recurrent LFA structure is carefully designed with the incorporation of HOI, thereby improving the representa-tion learning ability of a resultant model. Experimental results on three real-world datasets demonstrate that GLFA outperforms six state-of-the-art models in predicting the missing data of an HiDS matrix, which evidently supports its strong representation learning ability to HiDS data.

Deep Learning has implemented a wide range of applications and has become increasingly popular in recent years. The goal of multimodal deep learning is to create models that can process and link information using various modalities. Despite the extensive development made for unimodal learning, it still cannot cover all the aspects of human learning. Multimodal learning helps to understand and analyze better when various senses are engaged in the processing of information. This paper focuses on multiple types of modalities, i.e., image, video, text, audio, body gestures, facial expressions, and physiological signals. Detailed analysis of past and current baseline approaches and an in-depth study of recent advancements in multimodal deep learning applications has been provided. A fine-grained taxonomy of various multimodal deep learning applications is proposed, elaborating on different applications in more depth. Architectures and datasets used in these applications are also discussed, along with their evaluation metrics. Last, main issues are highlighted separately for each domain along with their possible future research directions.

The essence of multivariate sequential learning is all about how to extract dependencies in data. These data sets, such as hourly medical records in intensive care units and multi-frequency phonetic time series, often time exhibit not only strong serial dependencies in the individual components (the "marginal" memory) but also non-negligible memories in the cross-sectional dependencies (the "joint" memory). Because of the multivariate complexity in the evolution of the joint distribution that underlies the data generating process, we take a data-driven approach and construct a novel recurrent network architecture, termed Memory-Gated Recurrent Networks (mGRN), with gates explicitly regulating two distinct types of memories: the marginal memory and the joint memory. Through a combination of comprehensive simulation studies and empirical experiments on a range of public datasets, we show that our proposed mGRN architecture consistently outperforms state-of-the-art architectures targeting multivariate time series.

Graph neural networks (GNNs) are a popular class of machine learning models whose major advantage is their ability to incorporate a sparse and discrete dependency structure between data points. Unfortunately, GNNs can only be used when such a graph-structure is available. In practice, however, real-world graphs are often noisy and incomplete or might not be available at all. With this work, we propose to jointly learn the graph structure and the parameters of graph convolutional networks (GCNs) by approximately solving a bilevel program that learns a discrete probability distribution on the edges of the graph. This allows one to apply GCNs not only in scenarios where the given graph is incomplete or corrupted but also in those where a graph is not available. We conduct a series of experiments that analyze the behavior of the proposed method and demonstrate that it outperforms related methods by a significant margin.

小貼士

登錄享

相關主題

注冊地址: 北京市海淀區羊坊店路18號2幢3層301-191