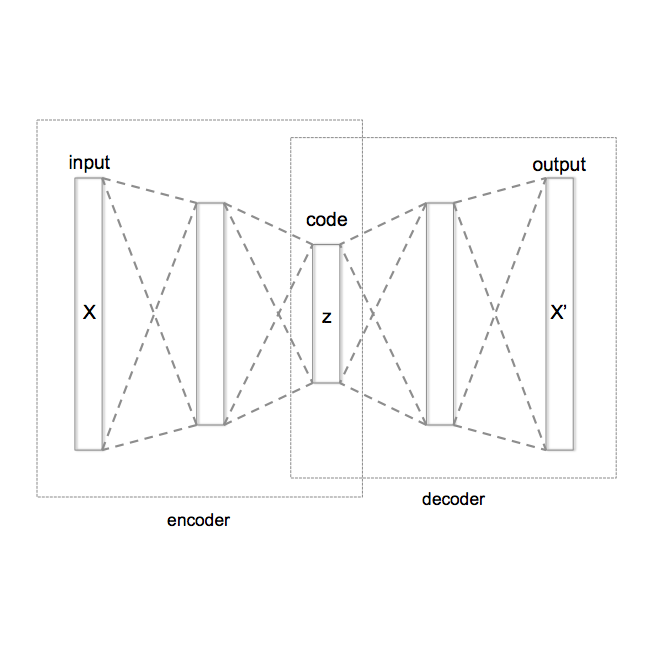

In this research, we propose a novel approach for the quantification of credit portfolio Value-at-Risk (VaR) sensitivity to asset correlations with the use of synthetic financial correlation matrices generated with deep learning models. In previous work Generative Adversarial Networks (GANs) were employed to demonstrate the generation of plausible correlation matrices, that capture the essential characteristics observed in empirical correlation matrices estimated on asset returns. Instead of GANs, we employ Variational Autoencoders (VAE) to achieve a more interpretable latent space representation. Through our analysis, we reveal that the VAE latent space can be a useful tool to capture the crucial factors impacting portfolio diversification, particularly in relation to credit portfolio sensitivity to asset correlations changes.

相關內容

This brief addresses the design of a Nonlinear Model Predictive Control (NMPC) strategy for exponentially incremental Input-to-State Stable (ISS) systems. In particular, a novel formulation is devised, which does not necessitate the onerous computation of terminal ingredients, but rather relies on the explicit definition of a minimum prediction horizon ensuring closed-loop stability. The designed methodology is particularly suited for the control of systems learned by Recurrent Neural Networks (RNNs), which are known for their enhanced modeling capabilities and for which the incremental ISS properties can be studied thanks to simple algebraic conditions. The approach is applied to Gated Recurrent Unit (GRU) networks, providing also a method for the design of a tailored state observer with convergence guarantees. The resulting control architecture is tested on a benchmark system, demonstrating its good control performances and efficient applicability.

In this paper, we show that the Kolmogorov two hidden layer neural network model with a continuous, discontinuous bounded or unbounded activation function in the second hidden layer can precisely represent continuous, discontinuous bounded and all unbounded multivariate functions, respectively.

In this paper, we consider robust nonparametric regression using deep neural networks with ReLU activation function. While several existing theoretically justified methods are geared towards robustness against identical heavy-tailed noise distributions, the rise of adversarial attacks has emphasized the importance of safeguarding estimation procedures against systematic contamination. We approach this statistical issue by shifting our focus towards estimating conditional distributions. To address it robustly, we introduce a novel estimation procedure based on $\ell$-estimation. Under a mild model assumption, we establish general non-asymptotic risk bounds for the resulting estimators, showcasing their robustness against contamination, outliers, and model misspecification. We then delve into the application of our approach using deep ReLU neural networks. When the model is well-specified and the regression function belongs to an $\alpha$-H\"older class, employing $\ell$-type estimation on suitable networks enables the resulting estimators to achieve the minimax optimal rate of convergence. Additionally, we demonstrate that deep $\ell$-type estimators can circumvent the curse of dimensionality by assuming the regression function closely resembles the composition of several H\"older functions. To attain this, new deep fully-connected ReLU neural networks have been designed to approximate this composition class. This approximation result can be of independent interest.

Recently, partial Bayesian neural networks (pBNNs), which only consider a subset of the parameters to be stochastic, were shown to perform competitively with full Bayesian neural networks. However, pBNNs are often multi-modal in the latent-variable space and thus challenging to approximate with parametric models. To address this problem, we propose an efficient sampling-based training strategy, wherein the training of a pBNN is formulated as simulating a Feynman--Kac model. We then describe variations of sequential Monte Carlo samplers that allow us to simultaneously estimate the parameters and the latent posterior distribution of this model at a tractable computational cost. We show on various synthetic and real-world datasets that our proposed training scheme outperforms the state of the art in terms of predictive performance.

For multi-scale problems, the conventional physics-informed neural networks (PINNs) face some challenges in obtaining available predictions. In this paper, based on PINNs, we propose a practical deep learning framework for multi-scale problems by reconstructing the loss function and associating it with special neural network architectures. New PINN methods derived from the improved PINN framework differ from the conventional PINN method mainly in two aspects. First, the new methods use a novel loss function by modifying the standard loss function through a (grouping) regularization strategy. The regularization strategy implements a different power operation on each loss term so that all loss terms composing the loss function are of approximately the same order of magnitude, which makes all loss terms be optimized synchronously during the optimization process. Second, for the multi-frequency or high-frequency problems, in addition to using the modified loss function, new methods upgrade the neural network architecture from the common fully-connected neural network to special network architectures such as the Fourier feature architecture, and the integrated architecture developed by us. The combination of the above two techniques leads to a significant improvement in the computational accuracy of multi-scale problems. Several challenging numerical examples demonstrate the effectiveness of the proposed methods. The proposed methods not only significantly outperform the conventional PINN method in terms of computational efficiency and computational accuracy, but also compare favorably with the state-of-the-art methods in the recent literature. The improved PINN framework facilitates better application of PINNs to multi-scale problems.

In this paper we discuss a deterministic form of ensemble Kalman inversion as a regularization method for linear inverse problems. By interpreting ensemble Kalman inversion as a low-rank approximation of Tikhonov regularization, we are able to introduce a new sampling scheme based on the Nystr\"om method that improves practical performance. Furthermore, we formulate an adaptive version of ensemble Kalman inversion where the sample size is coupled with the regularization parameter. We prove that the proposed scheme yields an order optimal regularization method under standard assumptions if the discrepancy principle is used as a stopping criterion. The paper concludes with a numerical comparison of the discussed methods for an inverse problem of the Radon transform.

In this paper, we present an efficient solution for weed classification in agriculture. We focus on optimizing model performance at inference while respecting the constraints of the agricultural domain. We propose a Quantized Deep Neural Network model that classifies a dataset of 9 weed classes using 8-bit integer (int8) quantization, a departure from standard 32-bit floating point (fp32) models. Recognizing the hardware resource limitations in agriculture, our model balances model size, inference time, and accuracy, aligning with practical requirements. We evaluate the approach on ResNet-50 and InceptionV3 architectures, comparing their performance against their int8 quantized versions. Transfer learning and fine-tuning are applied using the DeepWeeds dataset. The results show staggering model size and inference time reductions while maintaining accuracy in real-world production scenarios like Desktop, Mobile and Raspberry Pi. Our work sheds light on a promising direction for efficient AI in agriculture, holding potential for broader applications. Code: //github.com/parikshit14/QNN-for-weed

The paper's goal is to provide a simple unified approach to perform sensitivity analysis using Physics-informed neural networks (PINN). The main idea lies in adding a new term in the loss function that regularizes the solution in a small neighborhood near the nominal value of the parameter of interest. The added term represents the derivative of the loss function with respect to the parameter of interest. The result of this modification is a solution to the problem along with the derivative of the solution with respect to the parameter of interest (the sensitivity). We call the new technique to perform sensitivity analysis within this context SA-PINN. We show the effectiveness of the technique using 3 examples: the first one is a simple 1D advection-diffusion problem to show the methodology, the second is a 2D Poisson's problem with 9 parameters of interest and the last one is a transient two-phase flow in porous media problem.

In this paper we develop a novel neural network model for predicting implied volatility surface. Prior financial domain knowledge is taken into account. A new activation function that incorporates volatility smile is proposed, which is used for the hidden nodes that process the underlying asset price. In addition, financial conditions, such as the absence of arbitrage, the boundaries and the asymptotic slope, are embedded into the loss function. This is one of the very first studies which discuss a methodological framework that incorporates prior financial domain knowledge into neural network architecture design and model training. The proposed model outperforms the benchmarked models with the option data on the S&P 500 index over 20 years. More importantly, the domain knowledge is satisfied empirically, showing the model is consistent with the existing financial theories and conditions related to implied volatility surface.

Recent advances in 3D fully convolutional networks (FCN) have made it feasible to produce dense voxel-wise predictions of volumetric images. In this work, we show that a multi-class 3D FCN trained on manually labeled CT scans of several anatomical structures (ranging from the large organs to thin vessels) can achieve competitive segmentation results, while avoiding the need for handcrafting features or training class-specific models. To this end, we propose a two-stage, coarse-to-fine approach that will first use a 3D FCN to roughly define a candidate region, which will then be used as input to a second 3D FCN. This reduces the number of voxels the second FCN has to classify to ~10% and allows it to focus on more detailed segmentation of the organs and vessels. We utilize training and validation sets consisting of 331 clinical CT images and test our models on a completely unseen data collection acquired at a different hospital that includes 150 CT scans, targeting three anatomical organs (liver, spleen, and pancreas). In challenging organs such as the pancreas, our cascaded approach improves the mean Dice score from 68.5 to 82.2%, achieving the highest reported average score on this dataset. We compare with a 2D FCN method on a separate dataset of 240 CT scans with 18 classes and achieve a significantly higher performance in small organs and vessels. Furthermore, we explore fine-tuning our models to different datasets. Our experiments illustrate the promise and robustness of current 3D FCN based semantic segmentation of medical images, achieving state-of-the-art results. Our code and trained models are available for download: //github.com/holgerroth/3Dunet_abdomen_cascade.

小貼士

登錄享

注冊地址: 北京市海淀區羊坊店路18號2幢3層301-191