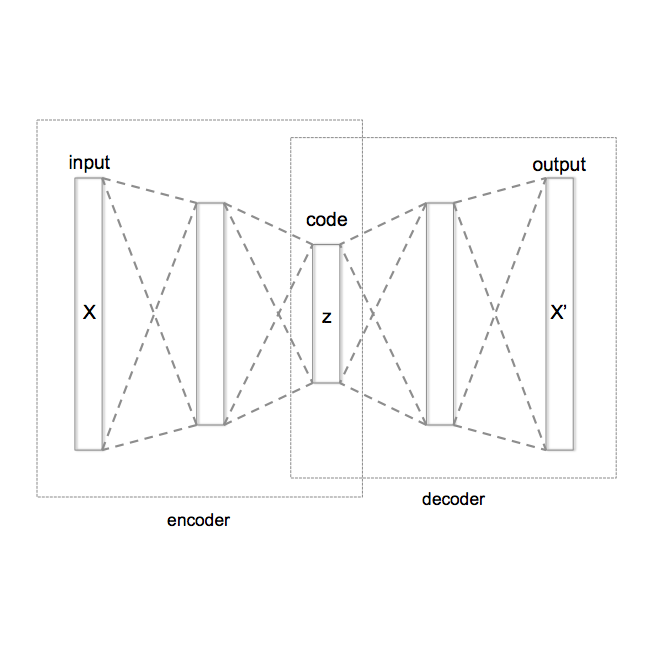

Factor model is a fundamental investment tool in quantitative investment, which can be empowered by deep learning to become more flexible and efficient in practical complicated investing situations. However, it is still an open question to build a factor model that can conduct stock prediction in an online and adaptive setting, where the model can adapt itself to match the current market regime identified based on only point-in-time market information. To tackle this problem, we propose the first deep learning based online and adaptive factor model, HireVAE, at the core of which is a hierarchical latent space that embeds the underlying relationship between the market situation and stock-wise latent factors, so that HireVAE can effectively estimate useful latent factors given only historical market information and subsequently predict accurate stock returns. Across four commonly used real stock market benchmarks, the proposed HireVAE demonstrate superior performance in terms of active returns over previous methods, verifying the potential of such online and adaptive factor model.

相關內容

Multivariate time series classification is a rapidly growing research field with practical applications in finance, healthcare, engineering, and more. The complexity of classifying multivariate time series data arises from its high dimensionality, temporal dependencies, and varying lengths. This paper introduces a novel ensemble classifier called RED CoMETS (Random Enhanced Co-eye for Multivariate Time Series), which addresses these challenges. RED CoMETS builds upon the success of Co-eye, an ensemble classifier specifically designed for symbolically represented univariate time series, and extends its capabilities to handle multivariate data. The performance of RED CoMETS is evaluated on benchmark datasets from the UCR archive, where it demonstrates competitive accuracy when compared to state-of-the-art techniques in multivariate settings. Notably, it achieves the highest reported accuracy in the literature for the 'HandMovementDirection' dataset. Moreover, the proposed method significantly reduces computation time compared to Co-eye, making it an efficient and effective choice for multivariate time series classification.

For safety-related applications, it is crucial to produce trustworthy deep neural networks whose prediction is associated with confidence that can represent the likelihood of correctness for subsequent decision-making. Existing dense binary classification models are prone to being over-confident. To improve model calibration, we propose Adaptive Stochastic Label Perturbation (ASLP) which learns a unique label perturbation level for each training image. ASLP employs our proposed Self-Calibrating Binary Cross Entropy (SC-BCE) loss, which unifies label perturbation processes including stochastic approaches (like DisturbLabel), and label smoothing, to correct calibration while maintaining classification rates. ASLP follows Maximum Entropy Inference of classic statistical mechanics to maximise prediction entropy with respect to missing information. It performs this while: (1) preserving classification accuracy on known data as a conservative solution, or (2) specifically improves model calibration degree by minimising the gap between the prediction accuracy and expected confidence of the target training label. Extensive results demonstrate that ASLP can significantly improve calibration degrees of dense binary classification models on both in-distribution and out-of-distribution data. The code is available on //github.com/Carlisle-Liu/ASLP.

Communication networks such as emails or social networks are now ubiquitous and their analysis has become a strategic field. In many applications, the goal is to automatically extract relevant information by looking at the nodes and their connections. Unfortunately, most of the existing methods focus on analysing the presence or absence of edges and textual data is often discarded. However, all communication networks actually come with textual data on the edges. In order to take into account this specificity, we consider in this paper networks for which two nodes are linked if and only if they share textual data. We introduce a deep latent variable model allowing embedded topics to be handled called ETSBM to simultaneously perform clustering on the nodes while modelling the topics used between the different clusters. ETSBM extends both the stochastic block model (SBM) and the embedded topic model (ETM) which are core models for studying networks and corpora, respectively. The inference is done using a variational-Bayes expectation-maximisation algorithm combined with a stochastic gradient descent. The methodology is evaluated on synthetic data and on a real world dataset.

In this paper, we conduct an empirical evaluation of Temporal Graph Benchmark (TGB) by extending our Dynamic Graph Library (DyGLib) to TGB. Compared with TGB, we include eleven popular dynamic graph learning methods for more exhaustive comparisons. Through the experiments, we find that (1) some issues need to be addressed in the current version of TGB, including mismatched data statistics, inaccurate evaluation metric computation, and so on; (2) different models depict varying performance across various datasets, which is in line with previous observations; (3) the performance of some baselines can be significantly improved over the reported results in TGB when using DyGLib. This work aims to ease the researchers' efforts in evaluating various dynamic graph learning methods on TGB and attempts to offer results that can be directly referenced in the follow-up research. All the used resources in this project are publicly available at //github.com/yule-BUAA/DyGLib_TGB. This work is in progress, and feedback from the community is welcomed for improvements.

Domain generalization (DG) aims to learn a robust model from source domains that generalize well on unseen target domains. Recent studies focus on generating novel domain samples or features to diversify distributions complementary to source domains. Yet, these approaches can hardly deal with the restriction that the samples synthesized from various domains can cause semantic distortion. In this paper, we propose an online one-stage Cross Contrasting Feature Perturbation (CCFP) framework to simulate domain shift by generating perturbed features in the latent space while regularizing the model prediction against domain shift. Different from the previous fixed synthesizing strategy, we design modules with learnable feature perturbations and semantic consistency constraints. In contrast to prior work, our method does not use any generative-based models or domain labels. We conduct extensive experiments on a standard DomainBed benchmark with a strict evaluation protocol for a fair comparison. Comprehensive experiments show that our method outperforms the previous state-of-the-art, and quantitative analyses illustrate that our approach can alleviate the domain shift problem in out-of-distribution (OOD) scenarios.

Multivariate functional data that are cross-sectionally compositional data are attracting increasing interest in the statistical modeling literature, a major example being trajectories over time of compositions derived from cause-specific mortality rates. In this work, we develop a novel functional concurrent regression model in which independent variables are functional compositions. This allows us to investigate the relationship over time between life expectancy at birth and compositions derived from cause-specific mortality rates of four distinct age classes, namely 0--4, 5--39, 40--64 and 65+. A penalized approach is developed to estimate the regression coefficients and select the relevant variables. Then an efficient computational strategy based on an augmented Lagrangian algorithm is derived to solve the resulting optimization problem. The good performances of the model in predicting the response function and estimating the unknown functional coefficients are shown in a simulation study. The results on real data confirm the important role of neoplasms and cardiovascular diseases in determining life expectancy emerged in other studies and reveal several other contributions not yet observed.

Unsupervised domain adaptation (UDA) provides a strategy for improving machine learning performance in data-rich (target) domains where ground truth labels are inaccessible but can be found in related (source) domains. In cases where meta-domain information such as label distributions is available, weak supervision can further boost performance. We propose a novel framework, CALDA, to tackle these two problems. CALDA synergistically combines the principles of contrastive learning and adversarial learning to robustly support multi-source UDA (MS-UDA) for time series data. Similar to prior methods, CALDA utilizes adversarial learning to align source and target feature representations. Unlike prior approaches, CALDA additionally leverages cross-source label information across domains. CALDA pulls examples with the same label close to each other, while pushing apart examples with different labels, reshaping the space through contrastive learning. Unlike prior contrastive adaptation methods, CALDA requires neither data augmentation nor pseudo labeling, which may be more challenging for time series. We empirically validate our proposed approach. Based on results from human activity recognition, electromyography, and synthetic datasets, we find utilizing cross-source information improves performance over prior time series and contrastive methods. Weak supervision further improves performance, even in the presence of noise, allowing CALDA to offer generalizable strategies for MS-UDA. Code is available at: //github.com/floft/calda

Sequential recommendation as an emerging topic has attracted increasing attention due to its important practical significance. Models based on deep learning and attention mechanism have achieved good performance in sequential recommendation. Recently, the generative models based on Variational Autoencoder (VAE) have shown the unique advantage in collaborative filtering. In particular, the sequential VAE model as a recurrent version of VAE can effectively capture temporal dependencies among items in user sequence and perform sequential recommendation. However, VAE-based models suffer from a common limitation that the representational ability of the obtained approximate posterior distribution is limited, resulting in lower quality of generated samples. This is especially true for generating sequences. To solve the above problem, in this work, we propose a novel method called Adversarial and Contrastive Variational Autoencoder (ACVAE) for sequential recommendation. Specifically, we first introduce the adversarial training for sequence generation under the Adversarial Variational Bayes (AVB) framework, which enables our model to generate high-quality latent variables. Then, we employ the contrastive loss. The latent variables will be able to learn more personalized and salient characteristics by minimizing the contrastive loss. Besides, when encoding the sequence, we apply a recurrent and convolutional structure to capture global and local relationships in the sequence. Finally, we conduct extensive experiments on four real-world datasets. The experimental results show that our proposed ACVAE model outperforms other state-of-the-art methods.

Graph Neural Networks (GNNs), which generalize deep neural networks to graph-structured data, have drawn considerable attention and achieved state-of-the-art performance in numerous graph related tasks. However, existing GNN models mainly focus on designing graph convolution operations. The graph pooling (or downsampling) operations, that play an important role in learning hierarchical representations, are usually overlooked. In this paper, we propose a novel graph pooling operator, called Hierarchical Graph Pooling with Structure Learning (HGP-SL), which can be integrated into various graph neural network architectures. HGP-SL incorporates graph pooling and structure learning into a unified module to generate hierarchical representations of graphs. More specifically, the graph pooling operation adaptively selects a subset of nodes to form an induced subgraph for the subsequent layers. To preserve the integrity of graph's topological information, we further introduce a structure learning mechanism to learn a refined graph structure for the pooled graph at each layer. By combining HGP-SL operator with graph neural networks, we perform graph level representation learning with focus on graph classification task. Experimental results on six widely used benchmarks demonstrate the effectiveness of our proposed model.

Multivariate time series forecasting is extensively studied throughout the years with ubiquitous applications in areas such as finance, traffic, environment, etc. Still, concerns have been raised on traditional methods for incapable of modeling complex patterns or dependencies lying in real word data. To address such concerns, various deep learning models, mainly Recurrent Neural Network (RNN) based methods, are proposed. Nevertheless, capturing extremely long-term patterns while effectively incorporating information from other variables remains a challenge for time-series forecasting. Furthermore, lack-of-explainability remains one serious drawback for deep neural network models. Inspired by Memory Network proposed for solving the question-answering task, we propose a deep learning based model named Memory Time-series network (MTNet) for time series forecasting. MTNet consists of a large memory component, three separate encoders, and an autoregressive component to train jointly. Additionally, the attention mechanism designed enable MTNet to be highly interpretable. We can easily tell which part of the historic data is referenced the most.

注冊地址: 北京市海淀區羊坊店路18號2幢3層301-191